Historically, understanding interest rate trends and cycles wasn’t deemed essential for multifamily or real estate investors. After all, interest rates had been on a consistent downtrend since the 1980s. However, this complacency, in retrospect, may have been slightly misguided.

Real estate investors, especially those in the multifamily sector, must now turn their attention to the macroeconomic shifts impacting interest rate landscapes. The forthcoming decades could very well differ from the patterns we’ve grown accustomed to over the past two decades.

It’s said that hindsight is always 20/20. While events prior to 2010 fall outside the purview of this discussion, it’s worth noting that even a cursory look at Economics 101 reveals a fundamental principle: when supply rises, prices will only increase if demand outpaces supply growth.

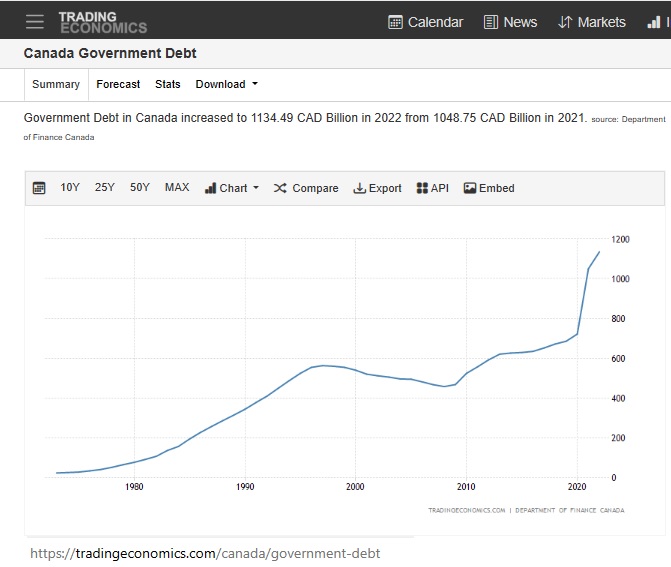

Take, for instance, Canada’s National Federal Debt. Since 2010, it has escalated from under $600 billion to over $1.3 trillion as of October 2023. A surge of over 100% in bond supply would typically result in higher yields.

Yet, contrary to expectations, interest rates for these bonds decreased during this period. For context, 5-year bond yields in Canada, which stood at over 3% in 2010, plummeted to a mere 0.38% by October 2020. This defied conventional wisdom and simultaneously led to a reduction in mortgage rates.

What’s the relevance of these developments for real estate investors?

Consider a hypothetical scenario wherein 5-year mortgage rates for multifamily loans had a spread of 100 basis points over the bond yield. A borrower between 2010 and 2020 could have witnessed an enhancement in their borrowing capacity by approximately 46%, solely due to the decline in mortgage rates from 4% to 1.4% – and all of this assuming consistent property value and net income.

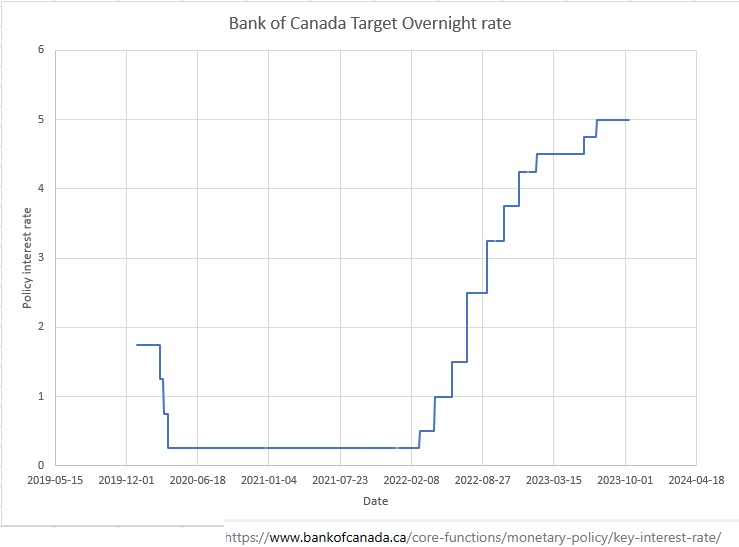

However, the dynamics have shifted dramatically post-2020. The Bank of Canada, mirroring steps taken by its global counterparts like the US Federal Reserve, began a cycle of rate hikes, raising the Overnight Policy rate from a mere 0.25% to a staggering 5% by July 2023. The purported rationale? Combating inflation. While central banks maneuver short-term rates, long-term bond yields, like the US Treasuries, or the 5 year Canada Savings Bonds are determined by the bond markets.

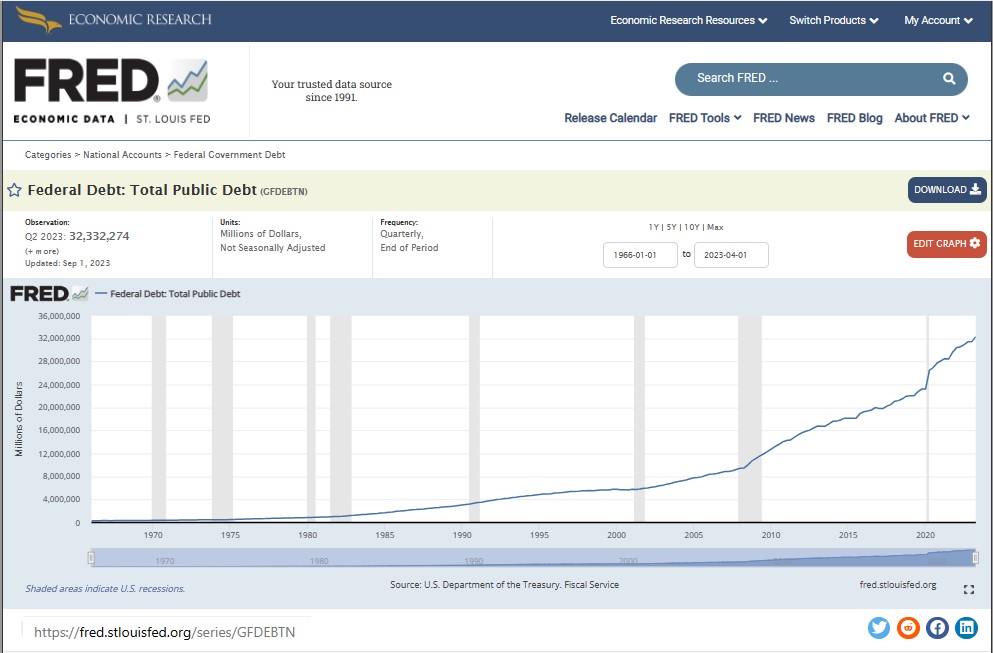

With the US National Debt at over $32 trillion and Canada’s at $1.3 trillion by Q2 2023, unchecked fiscal spending casts a shadow on the future. If this trajectory continues, a resurgence of lower interest rates seems implausible, particularly with anticipated inundation of bond markets due to government issuances.

So, how should real estate investors navigate this new terrain?

The key determinant of real estate value in this new paradigm will be net operating income. Previously, mere possession of a property and favorable interest and capitalization rates guaranteed appreciation. However, in an era of rising interest rates, if a property’s net operating income doesn’t evolve in tandem with interest rate spikes, its value will inevitably diminish. This fundamental shift necessitates a recalibration of strategies for all stakeholders in the real estate investment arena.